At NW Legacy Law, our estate planning lawyers understand that navigating the complexities of debt and estate matters can be daunting, especially during emotionally challenging times. One common question that arises is, "What happens to someone's debt when they die?" If you or your family has been faced with this situation, it's essential to grasp how debts are handled after death.

Does A Person's Debt Go Away When They Die?

When someone passes away, their debts do not simply disappear. The responsibility for these debts typically falls to their estate, which includes all the assets, property, and liabilities owned by the deceased at the time of their death. In Washington State, the process of managing a deceased person's debts involves several important steps.

The Role of the Executor

Typically, the court appoints an executor or personal representative to handle the deceased person’s estate. This individual is responsible for navigating what happens to someone's debt when they die, distributing assets, and ensuring that all legal obligations are met. If a person passes away with a will, the executor named in the will takes charge. Those without a will are managed under state intestacy laws, where the court appoints an administrator.

Inventory of Assets and Liabilities

The executor will begin by compiling an inventory of the deceased's assets and liabilities. This inventory should include real estate properties, bank accounts, investments, and any personal belongings of value. In Vancouver, local spots like the Columbia River waterfront or homes in the historic Fort Vancouver area may hold sentimental value but can also represent significant financial assets. Conversely, any debts incurred—like medical bills or personal loans—are documented as liabilities.

Payment of Debts

As per Washington State law, debts must be paid out of the estate before any distribution of assets to heirs or beneficiaries. This means that any remaining assets after debts are settled can be distributed according to the will or state intestacy laws. It’s essential to comprehend that if there are insufficient assets to cover the debts, the estate itself may be declared bankrupt, protecting the surviving family members from being liable for the debt. Personal debts, such as credit card balances, do not transfer to inheritors unless they were co-signed.

Secured Vs. Unsecured Debt

Secured debt is a type of loan backed by collateral, which reduces lender risk. If the borrower defaults, the lender can seize the pledged asset to recover their funds. Unsecured debt, by contrast, is not tied to any specific asset and relies solely on the borrower's creditworthiness.

Examples of Secured Debt include mortgages, auto loans, secured credit cards, and home equity loans. Examples of Unsecured debt include personal loans, credit card balances, student loans, and medical debt.

How These Debts Are Handled After Death

- Secured Debt: Assets used as collateral (like a house or car) may be:

- Sold to pay off the remaining balance

- Transferred to a heir who continues payments

- Repossessed by the lender if payments stop

- Unsecured Debt: Creditors file claims against the estate

- Debts are paid from the estate's assets in a specific legal order

- If the estate lacks sufficient funds, most unsecured debts typically go unpaid

- Heirs are generally not personally responsible for the deceased person's unsecured debts

How These Debts Are Handled After Death Infographic

What Happens If There Is No Estate?

What happens to someone's debt when they die when there aren't any assets (an "insolvent estate")? The debt resolution process becomes more complex. In most cases, if there are no assets to pay creditors, the majority of unsecured debts will simply go unpaid. Creditors typically cannot pursue payment from family members or heirs who are not joint account holders or cosigners.

Key Points for Insolvent Estates:

- Unsecured Debts: Most credit card debts, personal loans, and medical bills will be written off by creditors.

- Secured Debts: Lenders may repossess collateral (like a car or house) but cannot pursue additional payment.

- Exceptions: Debts that typically cannot be discharged include:

- Federal student loans (which may be forgiven upon death)

- Certain tax debts

- Child support or alimony obligations

Do Heirs Ever Have to Pay a Deceased Relative's Debt?

While heirs are typically not responsible for a deceased person's debts, there are specific circumstances where they may become liable:

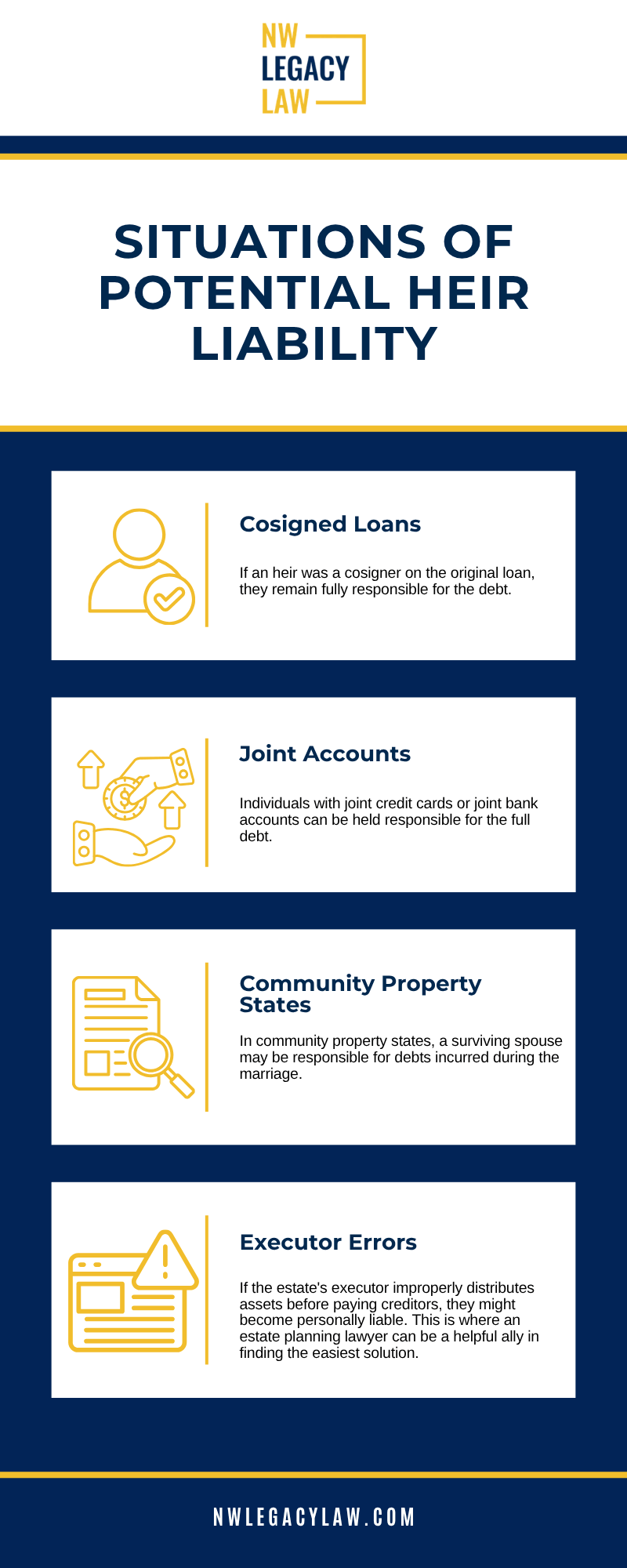

Situations of Potential Heir Liability:

- Cosigned Loans: If an heir was a cosigner on the original loan, they remain fully responsible for the debt.

- Joint Accounts: Individuals with joint credit cards or joint bank accounts can be held responsible for the full debt.

- Community Property States: In community property states (Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin), a surviving spouse may be responsible for debts incurred during the marriage.

- Executor Errors: If the estate's executor improperly distributes assets before paying creditors, they might become personally liable. This is where an estate planning lawyer can be a helpful ally in finding the easiest solution.

Scenarios Where Heirs Could Be at Risk:

- Failing to properly notify creditors during the probate process.

- Transferring assets before settling the deceased's outstanding debts.

- Accepting an inheritance that was intentionally structured to avoid creditor claims.

Limitations of Debt Collectors

When a person dies, their outstanding debts can create a complex and emotional challenge for grieving family members, which is why it's important to work with an estate planning lawyer. Debt collectors are bound by specific legal guidelines that restrict their communication and collection efforts regarding a deceased individual's financial obligations. Understanding these rules can help protect family members from undue stress and potential harassment during an already difficult time.

Who Debt Collectors Can Legally Contact:

- Executor or Personal Representative: The primary legal contact for settling the deceased's estate.

- Surviving Spouse: In community property states, or if they were a joint account holder.

- Cosigners on the Specific Debt: Legally responsible for the outstanding balance.

- Administrator of the Estate: The court-appointed individual managing the deceased's financial affairs.

Strict Limitations on Debt Collector Communication:

Collectors cannot:

- Harass or repeatedly contact other family members.

- Suggest other relatives are responsible for paying the debt.

- Claim family members must pay from their personal funds.

- Continue collection efforts after being informed of the death and provided estate contact information.

Washington State Protections

Washington State offers several important protections for families navigating what happens to someone's debt when they die, with specific legal provisions that can help shield heirs from undue financial burden.

Washington State Debt Collection Protections:

Community Property Considerations: Washington is a community property state, which means:

- Debts incurred during marriage may be considered joint obligations.

- Surviving spouses might be responsible for certain marital debts.

- However, separate debts incurred before marriage typically remain the deceased's sole responsibility.

Estate Settlement Protections:

Formal Probate Process: Provides a structured method for:

- Identifying and validating legitimate creditor claims

- Protecting heirs from improper debt collection attempts

- Ensuring orderly distribution of remaining assets

Statute of Limitations: Creditors have limited time to file claims against an estate (typically four months from the date of executor appointment) which prevents prolonged financial uncertainty for families.

Working With An Estate Planning Lawyer

Answering the question, "what happens to someone's debt when they die?", navigating debt collection, probate, and estate settlement requires specialized knowledge of Washington State laws. Without professional guidance, families risk inadvertently assuming unnecessary debt, mishandling asset distribution, or making legal missteps that could expose them to financial liabilities. Contact our estate planning lawyers at NW Legacy Law can help you understand your rights, verify creditor claims, and develop a strategic approach to estate management.